Gabriel Mihalache

International Economics

Welcome to my website; I study topics in International Economics and Macroeconomics. My work explores the consequences of sovereign default risk for the maturity structure of public debt, sectoral reallocation, capital accumulation, and fiscal-monetary interactions. I am an Assistant Professor of Economics at The Ohio State University. I received my PhD in 2016 from the University of Rochester. If you're curious, this is how you pronounce my last name.

Working Papers

- "Global Imbalances, Trade, and Sovereign Risk," Nov 2025

with Yan Bai, Minjie Deng, and Chang Liu

- "Sovereign Partial Default in Continuous Time," Feb 2024

with Sangdong Kim

- "The Maturity and Payment Schedule of Sovereign Debt," Jun 2016

with Yan Bai and Seon Tae Kim

Publications

- "Monetary Policy and Sovereign Risk in Emerging Economies (NK-Default),"

with Cristina Arellano and Yan Bai

The Quarterly Journal of Economics, 2026, 141(2), ISSN 0033-5533 - "Insufficient or Excessive Investment Under Sovereign Default Risk,"

with Ilhwan Song

Journal of International Economics, 2026, 160, ISSN 0022-1996 - "Default and Development,"

with Lei Li

Journal of International Economics, 2025, 155C, ISSN 0022-1996 - "Solving default models,"

Oxford Research Encyclopedia of Economics and Finance, 2025 - "Comment on `On Wars Sanctions and Sovereign Defaults' by Bianchi and Sosa-Padilla,"

Journal of Monetary Economics (C-R-NYU 100th Meeting), 2024, 141, ISSN 1873-1295 - "Deadly Debt Crises: COVID-19 in Emerging Markets,"

with Cristina Arellano and Yan Bai

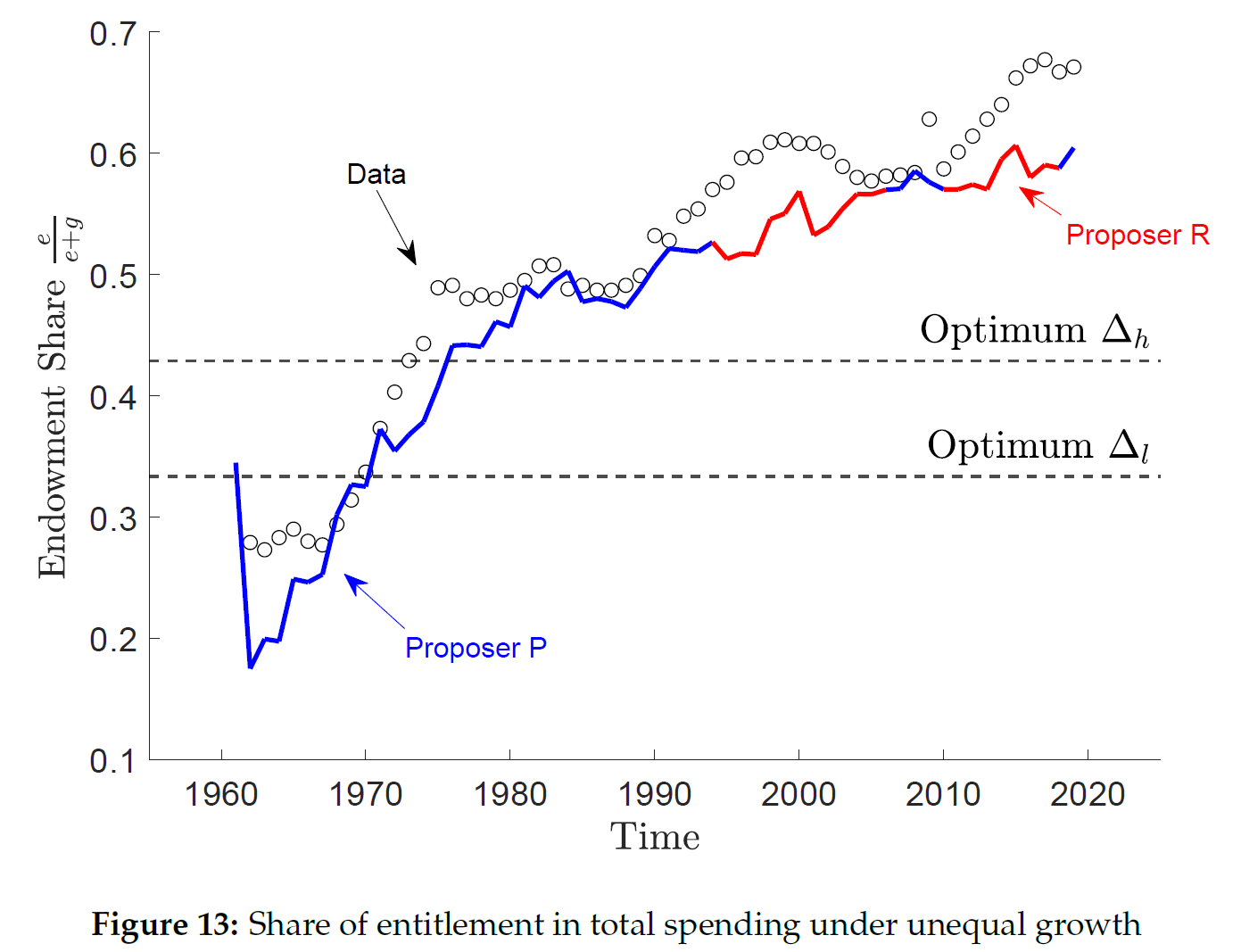

The Review of Economic Studies, 2023, 91(3), ISSN 0034-6527 - "Bargaining over Taxes and Entitlements in the Era of Unequal Growth,"

with Marina Azzimonti and Laura Karpuska

International Economic Review, 2023, 64(3), ISSN 0020-6598 - "COVID-19 Vaccination and Financial Frictions,"

with Cristina Arellano and Yan Bai

IMF Economic Review, 2023, 71(1), ISSN 2041-4161 - "Sovereign Default Resolution Through Maturity Extension,"

Journal of International Economics, 2020, 125C, ISSN 0022-1996 - "Default Risk, Sectoral Reallocation, and Persistent Recessions,"

with Cristina Arellano and Yan Bai

Journal of International Economics, 2018, 112, ISSN 0022-1996 - "The Payment Schedule of Sovereign Debt,"

with Yan Bai and Seon Tae Kim

Economics Letters, 2017, 161, ISSN 0165-1765

Resources

- Ohio Economy Dashboard: work-in-progress statistical forecasts

- US Debt Dashboard: debt-to-GDP, Macaulay duration, yields for the US

- Computation: Compilers, IDEs, languages, libraries for numerical methods

- Sovereign default reading list: key papers on quantitative models of (equilibrium) sovereign default

- A Fortran+MATLAB Workflow, for moving data or results back and forth

Teaching

All materials, including syllabi and recordings, are distributed via Carmen. Class-specific office hours are listed in the syllabus. For other appointments, please email. Students, please use mihalache.2@osu.edu and include the class name in the subject. Thank you!

Spring 2027

- ECON 5660 Financial Aspects of International Trade

- ECON 8862 International Economics 2 (PhD)

Previously

- ECON 4002.02 Intermediate Macroeconomics Theory

- ECON 5660 Financial Aspects of International Trade

- ECON 8862 International Economics 2 (PhD)

- At Stony Brook University:

- ECO 305 Intermediate Macroeconomic Theory

- ECO 325 International Trade

- ECO 386 International Finance

- ECO 531 Introduction to Computational Methods in Economics (MA)

- ECO 610 Advanced Macroeconomic Theory (PhD)

- ECO 613 Computational Macroeconomics (PhD)

Are you considering asking me to write a reference letter in support fo your grad school applications? Please read carefully the information available here, to help me help you. Thank you!

Personal